Ep.7 - Buy vs. Rent: How Much does It Really Cost to Own A Home?

📸 IG handle: DollarSenseLA

In episodes 1-4, I explained the four requirements you need to meet in order to buy a home in LA. Let's say you meet them all. You may still wonder, is it better to buy or keep on renting? I've got an answer for you.

Source: redfin.com; 4334 7th Ave,Los Angeles, CA 90008

The answer may surprise you. It is often times cheaper to own, due to two factors, tax deductions and equity building. I have owned my home for two years and I can speak with confidence in the numbers I am about to show. To best illustrate whether if it's cheaper to own, I am going to use the house I alluded to in episode 2. The 1608 sq ft house was sold for $650k in January 2017 in Leimert Park. If you don't remember what it looks like. The picture above should give you an idea (click on the picture itself for more details).

Nuance time! I am going to assume the buyers are a couple making at least $120,000 (if you wonder why, check out episode 2), and the house is financed with 5% down on a 30-year fixed conventional mortgage with an interest rate of 4.25%.

If you rent, there are only two components to your monthly costs, rent and utilities. However, the true cost of owning a home comes with two additional components, both are savings, in the forms of tax deductions and equity building. Both of these two components lower the cost of homeownership. To keep buying vs. renting in perspective, I will compare this Leimert Park house (1,600 sq ft) to three 2-bedroom apartments (800 to 1,200 sq ft; apartments tends to be smaller by default) in various places in LA. If you currently live in a 2-bedroom apartment in LA, I strongly encourage you to use your own rent as a benchmark.

Lincoln Place Apartments, Venice

Clarington Apartments, Culver City

Avalon Apartments, Playa Vista

Assumptions: buyers are a dual-income couple with income at least $120k. They purchased the $650k house with 5% down on a 4.25% fixed interest 30-year conventional loan

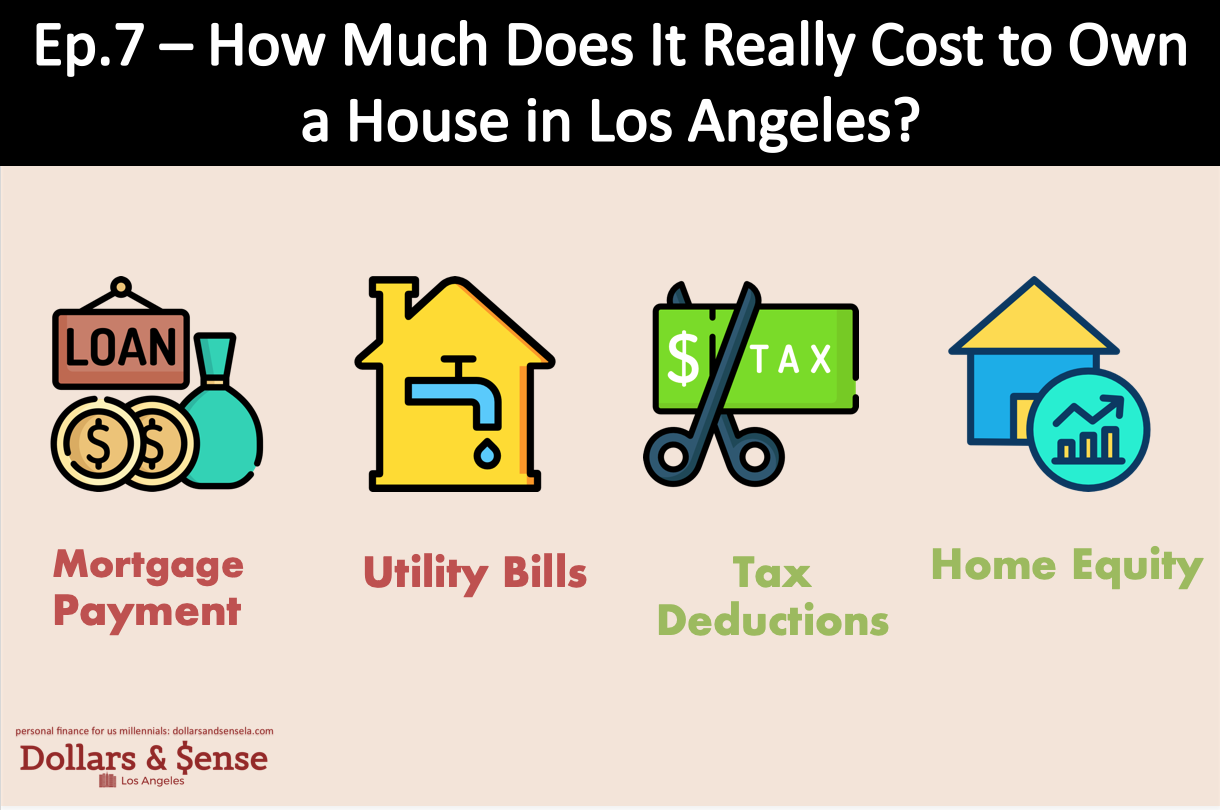

COMPONENT #1 : MORTGAGE/RENT

You Pay More Upfront Every Month When You Buy

It costs almost $4,000 a month to own this house in Leimert Park , while all the 2-bedroom apartments cost around $3,000. It is true that you will pay more upfront every month when you buy. If it is any consolation, the house is bigger and it has a yard. 😀

COMPONENT #2 : UTILITIES/MAINTENANCE

You Will Pay Around $300 More A Month

When you buy, your utility costs are significantly higher for two reasons. First, you are using more water/gas/electricity for a bigger space. Second, you are now paying for services that are usually covered by the landlord. These services include lawn care, water, trash, possibly ADT security.

Other than utility costs, your maintenance costs will also go up, as you essentially pay nothing for maintenance when you rent. While renting, the landlord takes care of all your apartment problems. If your food disposal is broken, the landlord will fix it. However, everything becomes your personal problem when you own. For example, since I moved into my house, I've had to replace my toilet valve, water faucet, sink dispenser, as well as doing some calking, patching, sanding and you name it.

COMPONENT #3: TAX DEDUCTIONS

You Get Around $10,000/year Back Through Tax Deductions

There are a number of tax deductions that make homeownership cheaper. The most common three are mortgage interest, property tax, and private mortgage insurance. Since I am assuming the couple buying this house has an income of +$120,000. The federal marginal tax rate is 25% and California tax rate is 9.3%, which combines to be 34.3%.

The couple pays $23,873 a year on mortgage interest. At the 34.3% marginal rate, they get back $8,188 in tax refund, which comes out to be $682 a month.

Similarly, the couple pays $7,800 a year on property tax. At the 34.3% marginal rate, they get back $2,675 in tax refund, which comes out to be $223 a month.

Private Mortgage Interest (PMI) is typically deductible, but not in this scenario, because it is entirely eliminated once the gross income (AGI) is over $109,000. In reality, first timers who are buying a house in LA need to make at least $120,000, hence making this deduction useless for the LA market. It's probably better to hear that from me now than having the wrong expectation later.

COMPONENT #4: EQUITY BUILDING

You are Paying Yourself and Building $800 Equity in the House

One key difference between buying and renting is that you own equity in the home you buy. And one day, you will own it outright without making any payment to anyone. For example, in the first year, when buying this house in Leimert Park, you are accruing roughly $795 a month in equity. As time goes on, you will accrue significantly more every month.

With everything accounted for, the true cost of owning this 1,608 sq ft house of $650k is $2,622, which is cheaper than all three apartments on my list. Again, you may be able to find a 2-bedroom apartment for less. But I doubt it will be much cheaper than $2,622.

SECRET WILD CARD: PROPERTY APPRECIATION

I've been comparing buy vs rent, excluding one important factor, property appreciation. Normally, over the long run, houses appreciate 3% - 5% a year. However, in the current LA market, the double digit home appreciation alone makes buying a better decision than renting, as many homes in LA have gone up by $100k in the past 2-3 years. Just Imagine how long it takes you to save up that much with your regular salary.

Property appreciation is a wild card, as no one can predict with certainty the housing market will stay hot in the 1, 3, 5, or 10 years. In my personal opinion, we have 3-5 years of continued appreciation here in LA. I will talk explain my thoughts in a future episode. But my guess is as good as any. For this reason, property appreciation has been left out of today's analysis.

NEXT EPISODE

As a millennial, we are all familiar with the word "debt". But have you ever thought about debt in relation to time? I think about debt as a time machine. It creates a temporal shift in your finances between the present self and your future self. Check back in next Friday, if you want to know why I call debt a time machine.

📸 IG handle: DollarSenseLA