Ep.72- How to Build a Personal Finance Budget

Read Time: 5 Minutes.

📸 IG handle: DollarSenseLA

New year, new start. If you want to have better control over your finances, there’s no better start than building out your personal budget. I’ve got the perfect budget tool to help you with that.

RYAN’S BUDGET TOOL:

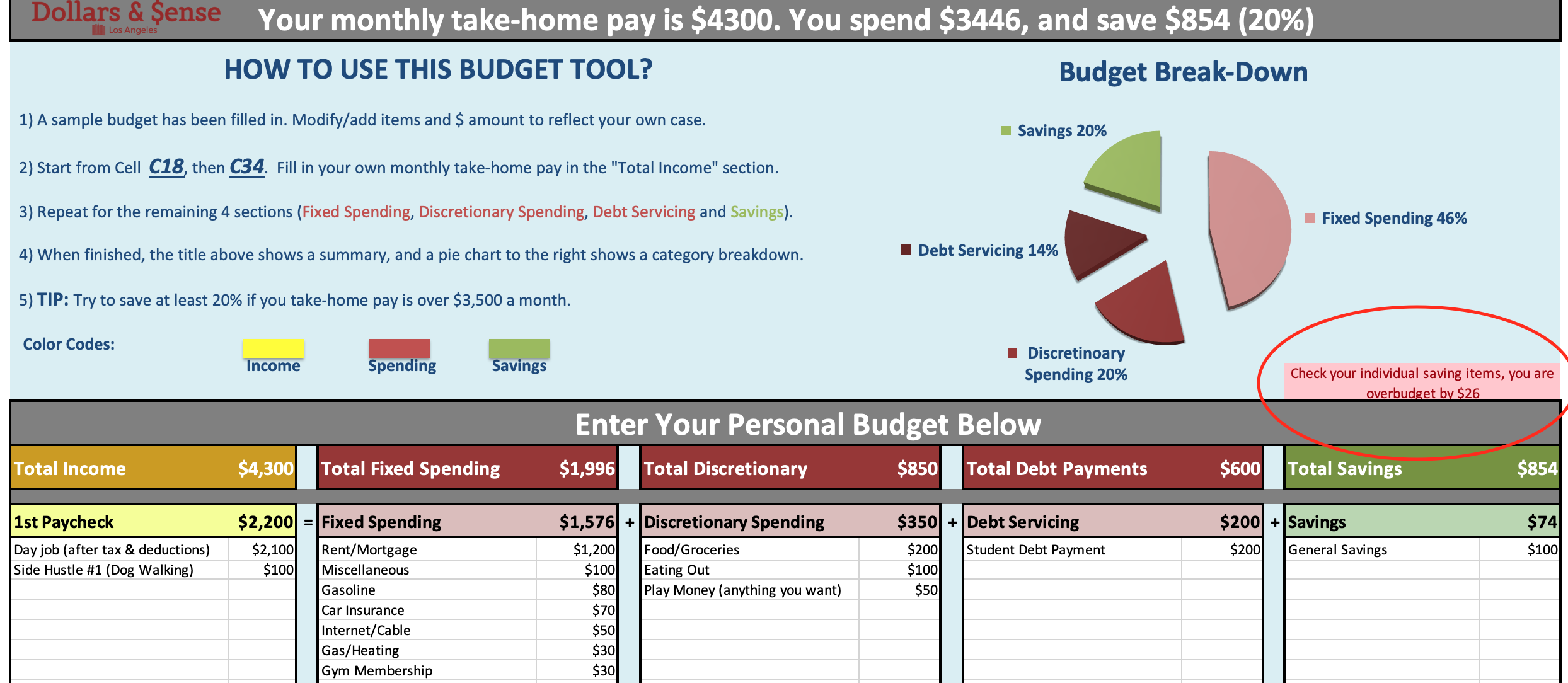

This is a newly designed budget tool I created for myself in 2019.

The budget tool is built to accommodate 2 paychecks per month, as most people get paid bi-weekly or semi-monthly. To help you get started, it’s been pre-filed with a sample budget of someone taking home $2,100 every pay period (after taxes and deductions). You need to modify/add based on your personal situation.

Before you start, let’s go over some budgeting basics.

BUDGETING BASICS

There are five components in a budget: Income, Fixed Spending, Discretionary Spending, Debt Servicing and Savings.

INCOME:

When I budget, I only treat income as post-tax, post-deduction take-home pay. This is the amount that's actually deposited to your bank account. For example, if you make $5000/month, you take home pay may only be $4000 or less. Use the $4000 number.

401k savings don't show up anywhere in my tool because this is an operational budget, and your 401k savings can't be spent yet.

Enter each additional income stream, such as your side hustle, in a separate line. If your income from your side hustle is not always steady like your day job, calculate the monthly average from the past 6 months.

FIXED SPENDING

Fixed spending refers to expenses that are recurring and relatively consistent month after month. The most common five are rent/mortgage, gasoline, auto insurance, utilities, and personal care.

One important item in this category we should all list out is "miscellaneous." It is a catch-all, covering one-off items you cannot easily forecast, such as car registration, replacing broken items, tipping the valet, paying for traffic tickets and etc. Life happens. Start with $100 each pay period.

DISCRETIONARY SPENDING

Discretionary spending is the type of spending where YOU have the flexibility to choose how much to spend. It typically includes three categories: groceries, eating out, and entertainment, which I call “play money”.

Groceries and eating out are highly correlated, because the more you cook, the less you will spend on eating out.

DEBT SERVICING

Debt is a dream crusher. The most common forms of debt (excluding mortgage) are auto loans, student loans, and credit card debt.

You should enter how much you can consistently pay, not just the minimum payment in the budget tool. If possible, put the payments on auto pay.

If you want to save every and pay a lump sum toward debt, you should budget that amount in the next section (Savings), NOT debt servicing.

SAVINGS

Savings is the money that's left over. Shoot for 20% of your take-home income. If you cannot save 20%, start by saving $100 a month, because it's an important habit to develop no matter how much you make.

If your budget isn’t balanced, a red section will popup, something like this one “check your individual saving items, you are over-budget by $x amount”. When this happens, you need to adjust your savings. When it’s balanced, the red section disappears.

For any purposeful savings, such as savings for a car, should be automatically transferred to a different account outside of your main checking account, so it prevents you from mixing money up and spending your savings.

TOP TIPS TO SAVE MORE

Lower your rent: This is THE single most effective driver on cutting down expenses. You can do so by moving in with more roommates, or further away, or live at home. It comes with its sacrifices, but there’s nothing else as effective as cutting out hundreds on rent.

Spend More on Groceries and Cook more: The second most effective way to save it to cook more, so you can eat out less. It’s ALWAYS cheaper to cook. For example, if you spend $200 more on your current groceries, you can most likely cut out +$400 of eating out.

Pick Up a Side Hustle: Start with this article on 84 lucrative side hustles. Often what stopping us from picking up a side hustle is pride. One may not want to drive for Uber and run into coworkers from his/her day job. I personally think there’s no shame in hustling. If you don’t feel comfortable, that’s also fine. You can pick up something else from the 84 things. Uber and Lyft are not the only options.

TL;DR

If you want to control your finances, there’s no better start than creating your own budget with Ryan’s budget tool.

There are five components in a budget: Income, Fixed Spending, Discretionary Spending, Debt Servicing and Savings. Your goal is to save at least 20%.

The single most effective way to save more is to lower rent. It could mean moving in with more roommates, moving further away, or temporarily living with the parents.