Ep.94- How to Manage Money in a Looming Recession

📸 IG handle: DollarSenseLA

The last 2 weeks have been a wild ride for the American economy. The WHO declared Covid-19 a global pandemic, the Federal Reserve lowered the interest rate by 50 basis points and decided to inject $1.5T into the market, Saudi and Russia sparked a crude oil flash crash, the Federal government declared a national emergency with a rescue package, most of the schools in America have closed, and a large amount of the American workforce is working from home now. Now the Federal reserve just dropped the interest rate and kicked off a round of Quantitative Easing on Sunday (March 15th 2020). The list goes on and on.

If I can sum up all of this into one chart, it would be this from the New York Times. For this reason, I am sharing my thoughts on how I think about managing my money during a looming recession.

VALUE PRESERVATION IS MY GOAL IN A LOOMING RECESSION

The first step of managing money in a looming recession to set the right goal. I personally believe the smart goal during a time like this is value preservation. What does value preservation mean in practice? For example, if you have $100k in your 401K, $20k in savings at this very moment, value preservation means you aim to still have the same amount, or something close, 12 months from now, something like $97k in 401k (a little loss realistically) and $20k in savings, even if the market crashes by 30%.

Some people preach this is a time to make massive gains. Personally I don’t think it is the right goal to set for 99% of us, because the average person can’t afford the risk that comes with the volatility. Perhaps if you are amongst the top 1%, you can afford to take the risk, since losing a $1 million would still not materially change anything in your life.

For the rest of us (outside of the top 1%), I laid out my thoughts on 4 actionable steps to help achieve value preservation in a bear market.

1. JOB SECURITY SHOULD BE YOUR HIGHEST PRIORITY

Having a steady income stream should be the absolute #1 priority, 1000x more important than anything that comes as a distant second.

Businesses are slowing down all over the world. How could it not when an entire city or country shuts down for weeks? It is inevitable that businesses, especially businesses that were already hugely unprofitable before, will struggle even after things resume to normal. When already struggling businesses reopen, the easiest thing to increase profit is to cut headcount. No one is entirely immune. I have seen layoffs from both Red Bull and BuzzFeed. One thing I learned is that it could impact as high up as a Senior Vice President, and as low as an entry-level contractor. It’s not personal, it’s strictly business, and it could happen to you.

The U.S lags behind China by 6 weeks in terms of the outbreak. Perhaps we can get a glimpse of the future through China. The video below from South China Morning Post shows that a layoff tends to happen after things get better, not necessarily during the outbreak. This is because, due to public perception and external pressure, businesses tend to do their best to have their employees paid at the peak of a crisis if they can. However, many workers receive a layoff letter the first day they return to work in the office, simply because businesses themselves ran out of money.

If you think your company will face significant financial difficulty in a recession, and you happen to be in a non-core role, such as in a support function, or a contracting position, you should look to transition to a core team or even look for an alternative elsewhere soon.

2. REBALANCE YOUR 401

As of 3/15/2020, I think you should shift at least 60% of your assets in your 401K to bonds. Here’s why, I am almost 100% certain we are not at the bottom yet, because the economic effect from city shutdowns, massive remote working, and business closure are just taking hold, and it will show up months down the road. Knowing the worst is yet to come with almost certainty, it makes sense to shift more assets into a safer place, bonds before the market drops further.

Personally I moved 100% of my 401k into bonds the end of February, which helped me mostly avoid the >20% drop. However, at this point, you don’t need to put 100% into bonds, because a lot of your losses have already taken place. However, it would be smart to shift at least a portion of your existing investment and future contribution into bonds. I think 60% bonds/40% stocks, is a good start.

I know the conventional wisdom is to not touch your 401k when the market is crashing. In general, I am not opposed to the idea, especially if we don’t know where the future holds. However, it does not make sense right now, because I am almost 100% certain (again almost) that we are not at the bottom yet.

A few people have asked me if they should move more into stocks. I think not. The worst is yet to come, and we almost know it for certain. It makes little sense to buy when you know it’s going down. I understand the past does not predict the future, however, history often sheds some light on what COULD happen.

As a reference, according to Market Watch, S&P usually drops >35% before it hits the lowest point (+50% in 2008), and it takes over 2 months, not 2 weeks to get there.

3. INCREASE YOUR EMERGENCY FUND SAVINGS BY 1 MONTH

You should cut spending right now, and beef up your emergency fund savings by 1 month. For example, if you have 1 month of savings, make it 2. If you have 4 months of savings, make it 5.

I understand asking everyone to increase savings to 6 months all of a sudden is not practical. However, if you are in a fortunate position of having six months of savings, you can afford to take some risks in a turbulent market (see step 4 below).

4. INVEST, BUT ONLY WITH EXTRA CASH

Chaos is a ladder. I know it sounds silly to quote from Game of Thrones. The next 12 months could be a good time to buy low, but only if you have the luxury of having extra uninvested cash, outside of your 6 months of the emergency fund.

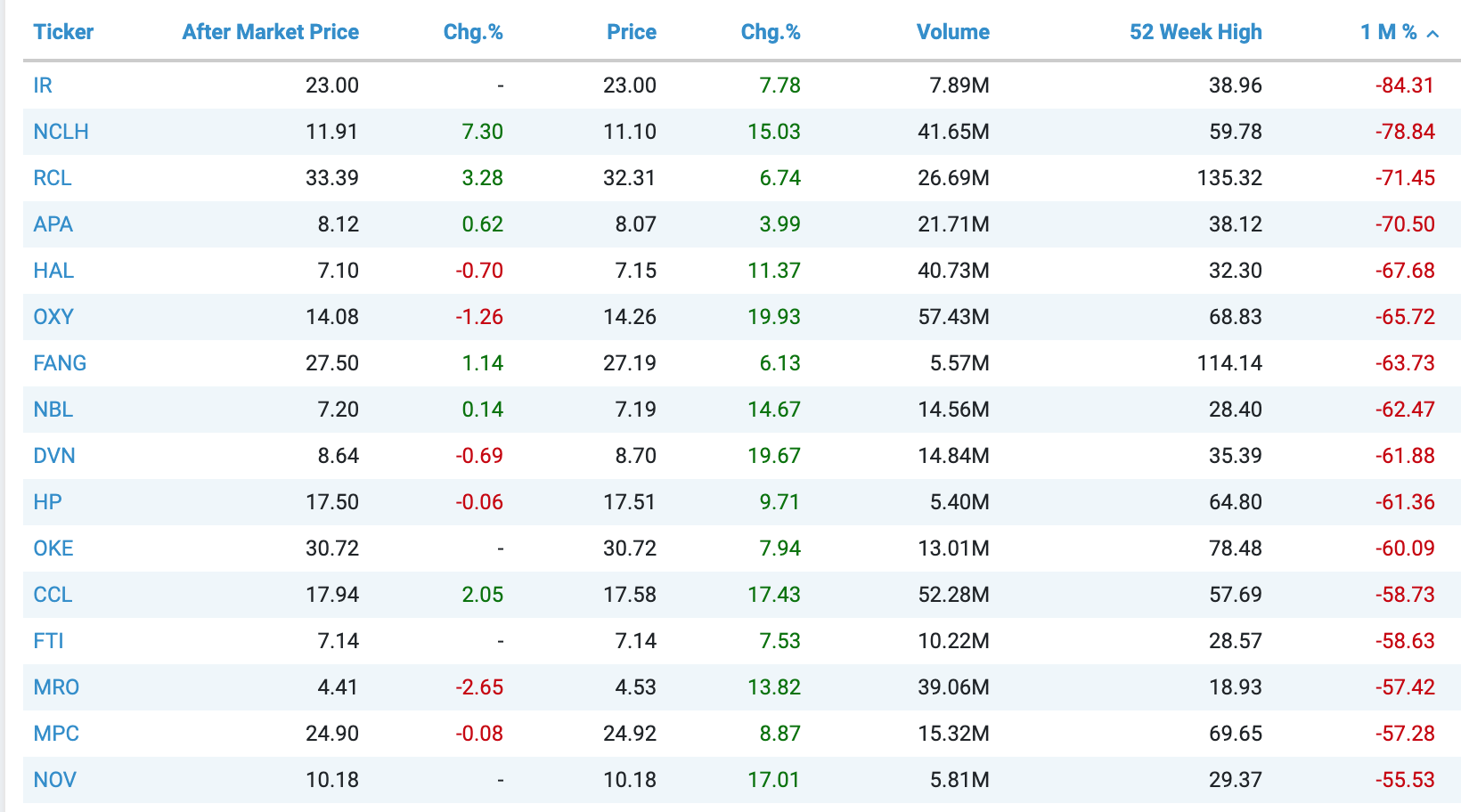

Many sectors have fallen significantly more (up to -80%) than the general market, particularly anything that’s hit hard by the coronavirus directly (see the chart below). This includes the cruise industry, airline industry, crude oil industry, and the entertainment industry. Some may go out of business and won’t rebound back even when the pandemic is over, while others will surge back as soon as pinned up demand is opened up again.

As far as I can see, crude oil and the airline industries are solid bets in the long run if you can hold it for years because the underlying demand is still there. When the crisis is over, people will fly again, and airlines will need more oil for their operations and etc. However, I am not so certain about the cruise stocks, as I think the demand will be down even after things resume to normal. Perhaps they will have to merge or risk being bought out in order to survive.

Stocks with the largest 1 month decline (within S&P 500)

IN CLOSING

In a looming recession, I believe in setting value preservation as the main goal, which simply means protecting the hard-earn money you already have. With that goal, your number 1 priority should be keeping a steady job, because it is foundational before you do anything else. If you don’t have a steady job, you will start to draw on your savings, and no investment return can easily replace your entire salary.